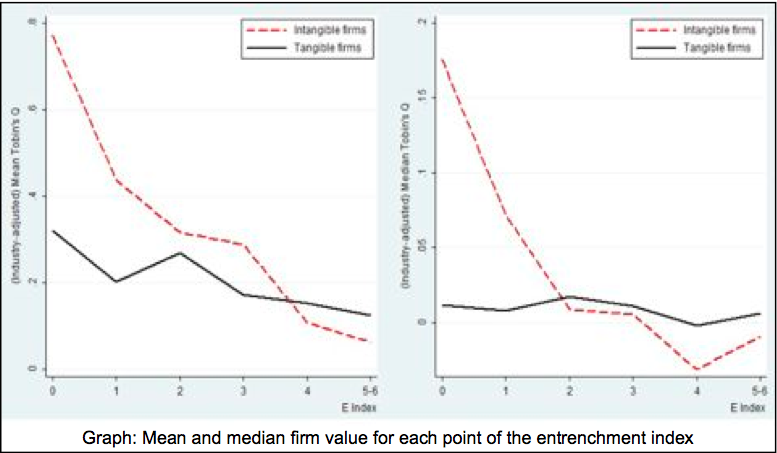

Intangible assets, which have grown rapidly on the balance sheet of firms in the last twenty years, are key sources of innovation and growth. They represent for instance more than 80% of US firms’ assets in the Hi-Tech or Pharmaceutical sector. In the article entitled “Takeover Discipline and Asset Tangibility”, I empirically study whether takeover vulnerability has a different effect on the performance of tangible and intangible firms. Background The corporate finance literature extensively mentions the role of takeovers in disciplining managers. Empirical evidence shows that managers are likely to be replaced in case of a takeover and that takeovers are more likely to occur in case of bad performance. The prospect of being fired following a takeover pushes ex ante managers to exert effort. Jensen in the 1980s has been a strong advocate of this positive view of takeovers, which received additional support in the seminal paper of Gompers, Ishii and Metrick (2003): they show that firms with less takeover defenses have on average higher firm value and equity returns. Results I use data on takeover defenses which are available for around 1500 listed US firms between 1990 and 2007, and construct the entrenchment index proposed by Bebchuk, Cohen and Ferrel (2009) which goes from 0 to 6 depending on the number of takeover defenses (among Classified Boards, limitations to amend bylaws, to amend the charter, supermajority for merger, poison pill and golden parachute) the firm has. I then measure firms’ asset tangibility with the ratio of property, plant and equipment over total assets, and rank firms as “tangible” or “intangible” firms. I obtain two results: first,, poor takeover vulnerability (high value of the entrenchment index) is associated with poor performance, but only so for intangible firms. If takeover discipline matters relatively more for the performance of intangible firms, shareholders of intangible firms are likely to be more active in fighting against the adoption of takeover defenses than shareholders of tangible firms. Consistent with this claim, I find that intangible firms have on average less takeover defenses than tangible firms. Antitakeover Laws Firm-level takeover defenses are likely to be endogenous. In particular, the positive association between takeover vulnerability and performance might be driven by the fact that managers of firms with low performance have incentives to adopt takeover defenses. In order to address endogeneity, I use the adoption of business combination (BC) laws as an exogenous shock to the market for corporate control. These laws were passed in 30 US states between 1985 and 1991 and generally impose a moratorium on mergers and asset sales between a large shareholder and a firm for a period usually ranging between three to five years after the shareholder’s stake reaches a pre-specified threshold. This moratorium makes in practice any hostile takeovers almost impossible. As previous studies, I find that firms’ operating performance drops after the laws’ passage. Then, once firms are sorted into tangible and intangible firms, I find that intangible firms protected by BC laws experience a significant drop in operating performance (around -1.4 percentage points) whereas tangible firms experience no significant effect. I obtain analogous results with event studies around the dates of the first newspaper reports about the BC laws. Stock prices react negatively to the announcement of BC laws only for intangible firms: cumulative abnormal returns equal -0.8% and are significant for intangible firms, whereas they are small and insignificant for tangible firms. Debt Discipline These findings suggest that takeover discipline matters only for intangible firms. My favorite explanation for these results is that tangible firms are already disciplined by debt. A large literature emphasizes the role of debt in mitigating agency problems between managers and investors.  First, debt limits managerial discretion by forcing the firm to disgorge cash flows. Debt discipline also rests on debtholders’ ability to exercise control when the firm defaults on its debt contract. Managers dislike default because they generally experience large salary and bonus reductions in that case. Ex ante, this gives them incentives to exert effort in order to avoid default.

However, debt is not an appropriate governance mechanism for intangible firms. Intangible firms have low liquidation values and low asset redeploy ability, and thus they might prefer to avoid debt and delegate monitoring to the market for corporate control. Alternative Stories I also examine another story which potentially explains the results. Takeover defenses or BC laws make takeovers less likely and thus reduce the probability that shareholders will receive premium as targets of an acquisition. If mergers and acquisitions (M&As) create on average more value in intangible than in tangible industries, this might explain for instance why stock prices of intangible firms react more at the announcement of a BC law. To address this point, I look directly at a sample of M&As: I find no evidence that industry asset tangibility drives the profitability of an acquisition. An alternative force is information asymmetry. The relative scarcity of public information on intangible firms makes good corporate governance a relatively more important issue for investors of these firms. Policy Overall, the evidence indicates that the appropriate disciplinary mechanism between debt and takeovers depends on the characteristics of the firm assets. This has important implications for governance design, suggesting for instance that owners of intangible firms should avoid installing takeover defenses at the IPO. References Bebchuk, Lucian A., Alma Cohen, and Allen Ferrell, 2009, What matters in corporate governance? Review of Financial Studies 22, 783-827. Bertrand, Marianne, and Sendhil Mullainathan, 2003, Enjoying the quiet life? Corporate governance and managerial preferences, Journal of Political Economy 111, 1043-1075. Field, Laura C., and Jonathan M. Karpo , 2002, Takeover defenses of IPO firms, Journal of Finance 57, 1857-1889. Gompers, P., J. Ishii, and A. Metrick, 2003, Corporate Governance and Equity Prices, Quaterly Journal of Economics 118, 107-155. Giroud, Xavier, and Holger M. Mueller, 2010, Does corporate governance matter in competitive industries? Journal of Financial Economics 95, 312-331.

0 Commentaires

Laisser une réponse. |

Archives

Octobre 2016

Categories

Tout

|

Flux RSS

Flux RSS